Over time, warrants have become a more common tool in company incentive programs. The purpose of warrants is to attract and retain employees by giving them a share of the upside. However, there are a number of pitfalls associated with the taxation of warrants. In this article, we dive into the taxation of warrants and the practical considerations for companies looking to implement warrant programs - and how to avoid the aforementioned pitfalls. The article focuses solely on employees and therefore not board members, investors and the like.

Update: New rules have been introduced regarding the taxation of warrants. We’ve written more about this in this article.

Warrants are a subscription right that gives the holder (employee) the right, but not the obligation, to subscribe (buy) shares in a company at a later date at a predetermined price. Warrants and options differ in that when a warrant is exercised, a new share is issued, while when an option is exercised, an already issued share is transferred.

When subscribing for the shares, the employee "exercises" their warrants, and the exercise price is already agreed at the time the employee is granted the warrants. The exercise price thereby remains locked in, and the employee is thus given the opportunity to purchase shares in the future at a potentially lower price than the market value at the time of exercise. After subscribing for the shares, the employee is thus a capital owner of the company.

Warrants can be particularly attractive as incentive schemes in startups and growth companies where liquidity may be limited and where a potential futureupsidemay be high. This can either be in the form of a sale(exit) or distribution of dividends.

Warrant programs are often structured so that the employee's warrants "mature"(vest) over a given period(the vesting period). During this period, the employee gradually earns the right to subscribe for more shares. The longer the employee works for the company, the more shares they are entitled to subscribe for.

It is not uncommon for a vesting period of 48 months (4 years) to be agreed, with warrants vesting linearly each month, however, so that the first 12 months vest all at once at the end of this period(cliff). The vesting period is typically linked to the employee's employment relationship. This means that the two periods typically follow each other. Therefore, if the employee terminates their employment, no further warrants will vest.

Example:

The number of matured warrants the employee can keep will also typically depend on the definition of the leaver provisions included in the warrant terms. For example, it is not unusual for an employee to lose the right to exercise matured and unmatured warrants if they are a bad leaver.

It can also happen that vesting is dependent on the company (or the employee) achieving a certain milestone. For example, the company and employees may agree that a portion of warrants will be vested if the company obtains a license, which is a prerequisite for the company to be able to sell its products - or for a salesperson, it may be that they must have established a certain number of customer relationships.

There are three events where it is relevant to consider taxation in relation to warrants: One is when warrants are granted, the second is when warrants are exercised to subscribe for shares and the third is when shares are sold for cash.

In general, employees are not taxed at the time the warrants are granted (even though the warrants represent a value and are typically granted free of charge). In this connection, it follows from sections 28 and 7 P of the Tax Assessment Act that taxation can be deferred to either the time of exercise (section 28) or the time of sale (section 7 P).

In order to apply sections 28 and 7 P of the Tax Assessment Act, it is a prerequisite that there is a real subscription right. This means that there must be a real possibility for a warrant holder to be "in the money", "at the money" or "out of the money". In practice, this means that you cannot set an exercise price that is so low that a warrant holder will certainly exercise their warrants. If the company sets an exercise price at, for example, DKK 0, the tax law reasoning is that the company could "just as well" allocate shares to the employee, which would trigger taxation.

In the following, we will go through sections 28 and 7 P and answer the questions raised by the provisions.

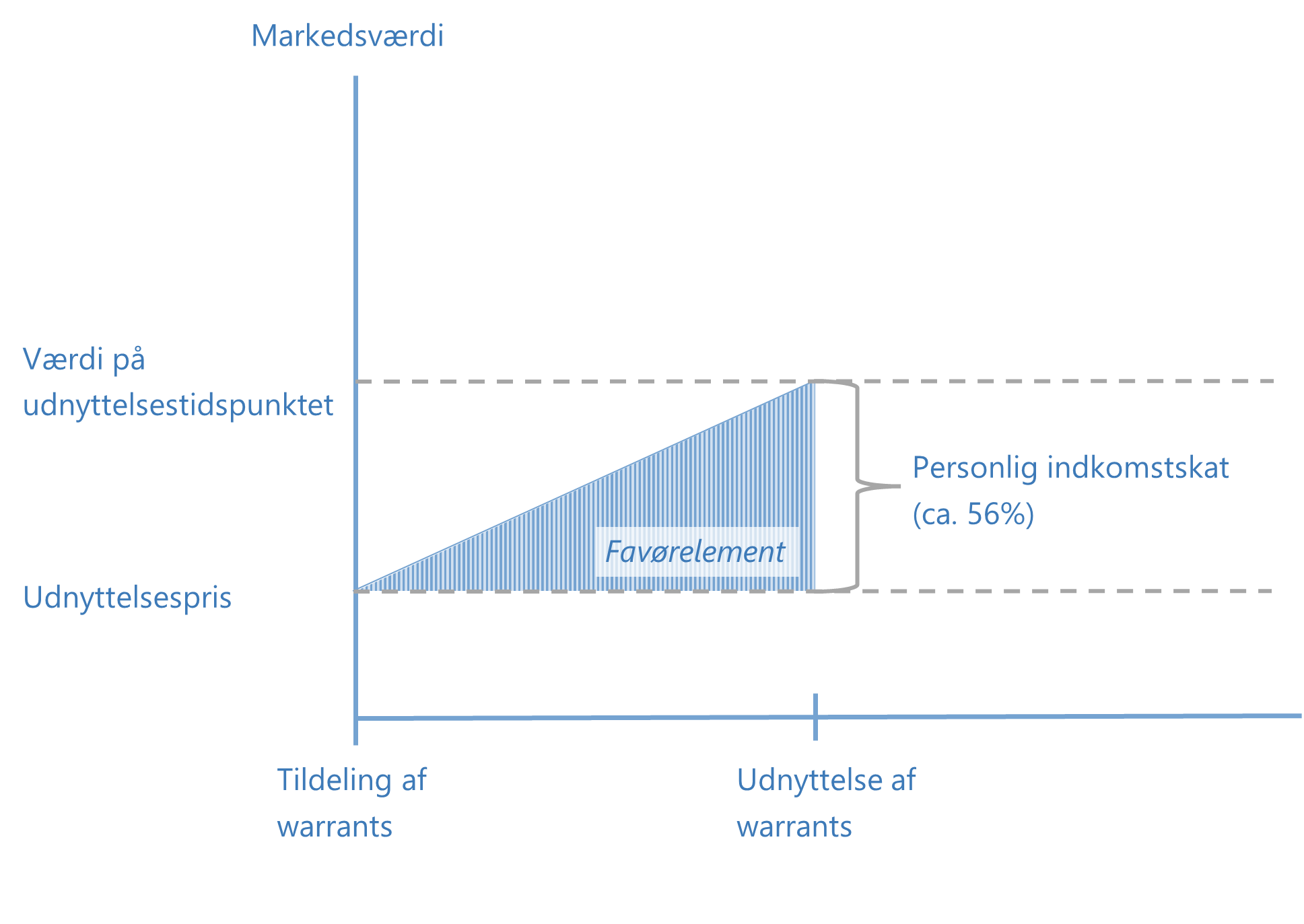

Section 28 of the Danish Taxation Act gives the employee the right to defer taxation until the time when the employee exercises their warrants. Taxation will then take place on the difference between the warrants' predetermined exercise price and the market price of the shares at the time of exercise - the difference between these two is also called the preferential element. The favor element is taxed as personal income, i.e. up to approx. 56% incl. AM contributions (payroll tax). Conversely, the company can deduct the favor element in its taxable income.

The favor element and its taxation can be illustrated as follows:

If the exercise price of the warrants is DKK 100 and the value of the shares at the time of exercise is DKK 300, the preferential element consists of DKK 200. According to section 28, the employee must be taxed on this amount as salary income, while the company can deduct it from its taxable income.

When the employee subsequently sells the shares acquired through the exercise of warrants, the gain is taxed as share income. Taxation will then be based on the difference between the value of the shares at the time of warrant exercise and the actual sale price of the shares. The first DKK 67,500 (2025) is taxed at a rate of 27%, after which the rest is taxed at a rate of 42%.

The taxation when selling the shares can be illustrated as follows:

When granting warrants, the company must report this to the Tax Agency via eIncome. When the employee exercises their warrants and subscribes for shares, the company must report via both eIncome and eCapital (AKSA reporting).

There are the following advantages and disadvantages associated with section 28 of the Tax Assessment Act.

Benefits:

Disadvantages:

Example of taxation according to section 28 of the Tax Assessment Act:

An employee is granted 500 warrants with an exercise price of DKK 100 per warrant. No taxable event occurs at this time.

After 4 years, the market value per share is DKK 400 and the employee exercises all his warrants. The employee pays his exercise price of DKK 50,000 (DKK 100 x 500 warrants), subscribes for the shares and becomes a shareholder of the company. At the same time, a taxable event occurs on the benefit element of DKK 150,000 ((DKK 400 x 500 shares) - (DKK 100 x 500 warrants)), which at this time must be taxed as personal income.

Sub-example 1: Five years after acquiring the shares, the employee chooses to sell them, triggering another tax liability for the employee. At this point, the market value of the shares has increased to DKK 800 per share and the gain of DKK 200,000 ((DKK 800 x 500 shares) - (DKK 400 x 500 shares)) is taxed as share income.

Sub-example 2: Five years after the acquisition of the shares, their value has decreased to 0. The employee has thus paid personal income tax on DKK 150,000 without having realized any value.

Exit warrants

As described below, the disadvantage of section 7 P is that there is an upper limit to the number of warrants that can be taxed under this provision. This is not the case for section 28. Therefore, it is not uncommon for companies to structure their warrant program under section 28 as so-called exit warrants.

In practice, employees are granted warrants under section 28 with a long exercise period of, for example, 20 years. The logic is that the company will most likely be sold(exit) within this period, and the employees can exercise their warrants in connection with such a sale. Because the exercise of the warrants and the sale of the shares occur simultaneously, the employees ensure that their shares do not fall drastically in price immediately after the exercise.

The advantage for the employees is that they do not risk being taxed on an unrealized gain, while the disadvantages are that they are taxed on the entire gain as salary income, and that they do not become capital owners and thus become entitled to any dividend distribution. For the company, the disadvantage is that it cannot deduct the preferential element in its taxable income.

The rule in section 7 P gives the employee the right to defer taxation until the time when the employee sells the shares for cash. The taxation will then be on the difference between the exercise price of the warrants and the actual sale price of the shares and as share income.

The taxation can be illustrated as follows:

.png)

It must be agreed in writing between the company and the employee that section 7 P of the Tax Assessment Act is applied, and when the warrants are allocated, the company must report the allocation to the Tax Agency via eIncome. When the employee exercises his warrants and subscribes for shares, the company must report to eKapital (AKSA reporting).

There are the following advantages and disadvantages associated with section 7 P of the Tax Assessment Act.

Benefits:

Disadvantages:

10%, 20% and 50% rules under section 7 P of the Tax Assessment Act:

There are three limits for the value of the warrants that can be granted under section 7 P. The limits are 10%, 20% and 50% and relate to the employee's annual salary at the time of grant.

For the 10% and 20% limits, a step-by-step structure applies, where 20% requires that the conditions for 10% are met. Access to the 50% limit, on the other hand, is independent of the other levels.

In order to apply § 7 P, the following applies:

Example:

An employee with an annual salary of DKK 600,000 receives warrants corresponding to 10% of the annual salary, including for example 500 warrants with an exercise price of DKK 100 per warrant. A taxable event does not occur at this time.

After 4 years, the market value per share is DKK 400 and the employee exercises all his warrants. The employee pays his exercise price of DKK 50,000 (DKK 100 x 500 warrants), subscribes for the shares and becomes a shareholder of the company. A taxable event still does not occur at this point.

It is important to note that the conditions for the 10% limit are still met despite the increase in market value, as the assessment of the warrants' value is based on the grant date.

Five years after acquiring the shares, the employee chooses to sell them and taxation does not start until then. At this point, the market value of the shares has increased to DKK 800 per share and the gain of DKK 350,000 ((DKK 800 x 500 shares) - (DKK 100 x 500 shares)) is taxed as share income.

New rules will remove the value restriction under section 7 P:

On August 25, 2025, the government has sent a bill for consultation that entails significant changes to section 7 P of the Tax Assessment Act. Among other things, the bill proposes that the current value limitation of 50% of the employee's annual salary is abolished. Instead, companies will be able to grant an unlimited number of warrants under section 7 P of the Tax Assessment Act and thus income tax-free, provided that the employee receives an annual salary corresponding to at least the unemployment benefit rate (approximately DKK 253,000 in 2025).

The changes are proposed to enter into force on January 1, 2026. The entry into force is conditional on the bill being adopted by the Danish Parliament and approved by the European Commission under the state aid rules. Until then, the current rules with value limits of 10%, 20% and 50% apply. Our article about the bill can be read here.

To establish an effective warrant program, companies should focus on designing a structure that supports the company's strategic goals while motivating employees. The choice between sections 28 and 7 P of the Tax Assessment Act depends on what best benefits both employees and the company, as they have different tax advantages.

Basically, Section 7 P is an advantage for the employee because you are only taxed on the amount you actually earn. On the other hand, it is often difficult to be sure if you are covered by section 7P. The reason for this is that there is a cap on the number of warrants that are taxed by section 7 P and that a value calculation of the warrants in question must be made. The different valuation methods give very different results, and it is often difficult to determine which valuation method to use.

If section 28 is used instead, the risk of taxation of an unrealized value can be countered by structuring the scheme as so-called exit warrants as described above. The characteristic feature of exit warrants is that the shares are sold immediately after the warrants are exercised. This means that the employee does not bear the risk of a loss of value in the shares. However, as mentioned above, this also means that the employee does not become a capital owner along the way and thus does not receive any dividends before an exit, just as the employee has no management rights in the company (voting rights).

The decision on the warrant program must be approved at the general meeting and relevant company law documents must be prepared and registered correctly. At the same time, it is important to communicate clearly with employees so that they understand both the benefits and tax consequences of warrants, as the taxation of warrants is a matter that belongs to the employee. It is therefore also crucial that all agreements are in writing and clearly define the terms of grant and exercise.

Establishing a warrant program therefore requires planning and insight into legal, employment law and tax aspects. The process includes development and implementation for ongoing administration and ensuring compliance with applicable rules. You can read more about the specific process here.